Get the best data-driven crypto insights and analysis every week:

By: Tanay Ved

-

MicroStrategy operates as a Bitcoin treasury company and a leveraged proxy to Bitcoin, amplifying BTC’s price movements both on the upside and downside.

-

The company now holds 386,700 BTC (valued at ~$36B), representing 1.9% of Bitcoin’s current supply—making them the largest corporate holder of BTC globally.

-

MicroStrategy funds its Bitcoin acquisitions through convertible bonds, capitalizing on low borrowing costs and elevated equity premiums during bull markets to expand its BTC holdings.

Bitcoin’s post-election momentum has pushed it toward the $100K mark for the first time in its 15-year history. While much of its supply remains self-custodied, Bitcoin’s growing maturity has unlocked more accessible investment avenues, including “crypto equities”—publicly traded stocks that provide exposure or a proxy to Bitcoin and other digital assets via traditional brokerage accounts. These range from Bitcoin miners like Marathon Digital (MARA) to full-stack operators like Coinbase (COIN) and MicroStrategy (MSTR), the largest corporate holder of Bitcoin with 386,700 BTC in its treasury. The launch of spot Bitcoin (BTC) and Ether (ETH) ETFs this year has further broadened institutional access.

In this week’s issue of Coin Metrics’ State of the Network, we analyze MicroStrategy’s performance, its Bitcoin holdings, and its role as a leveraged proxy within the crypto equities landscape, exploring its acquisition strategy and the risks and rewards of its approach.

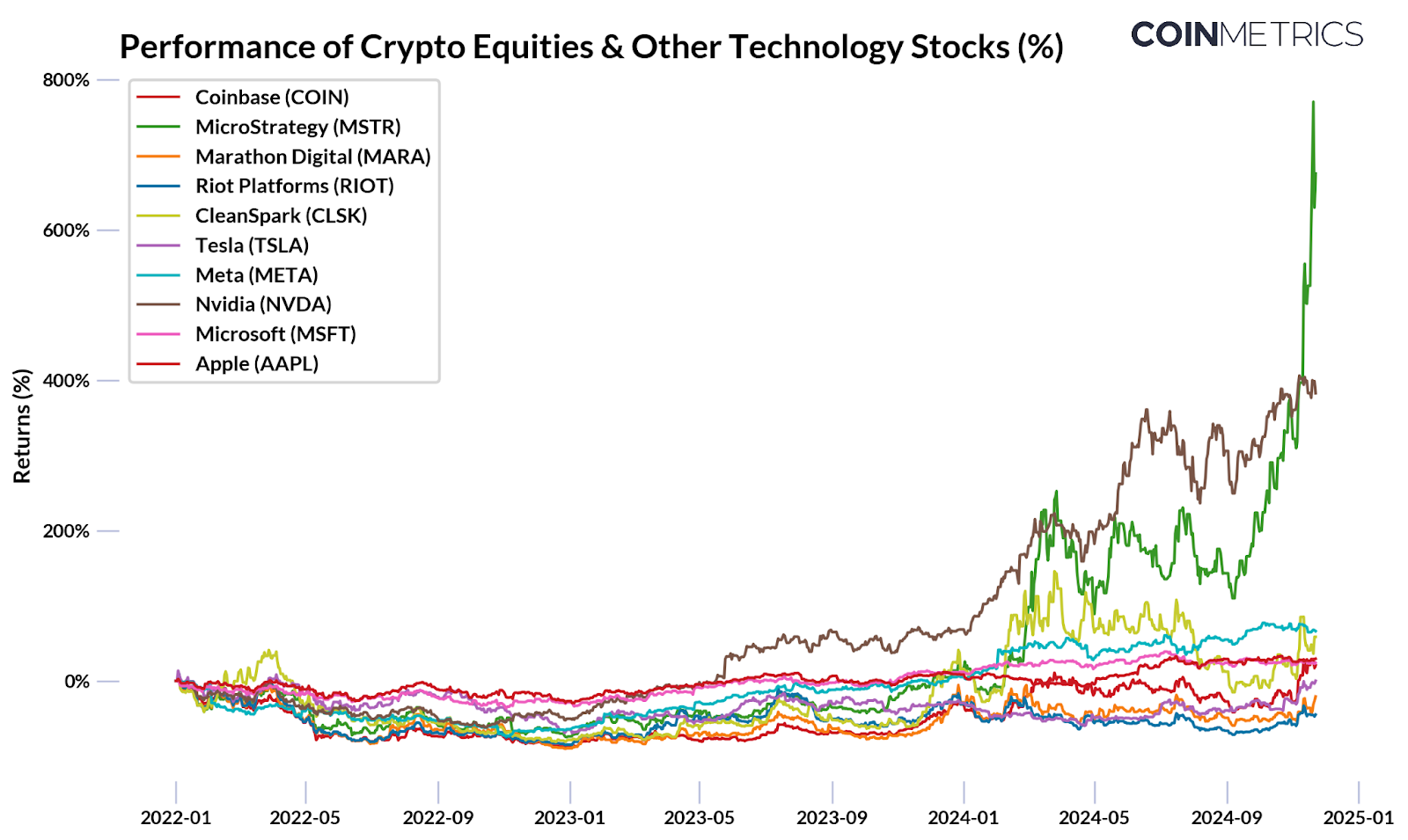

While MSTR is not a part of the S&P 500 index, it has delivered returns exceeding 700% since 2022 and 488% year-to-date, surpassing the performance of stocks within the S&P 500. Its performance far outpaces major crypto equities and technology stocks like Coinbase (COIN) or Nvidia (NVDA), driven by its unique role as a “Bitcoin treasury company”. Therefore, the strategy behind its performance warrants a closer look.

Source: Google Finance

Some may be surprised to learn that MicroStrategy was founded in 1989 as an enterprise software company specializing in business intelligence. However, in August 2020, co-founder and then-CEO Michael Saylor made a bold pivot, adopting Bitcoin as the company’s primary reserve asset as part of a “new capital allocation strategy.” This transformed MicroStrategy into a Bitcoin accumulation machine. Four years later, it has become the single largest corporate holder of Bitcoin, with 386,700 BTC (valued at ~$36B) and a market cap of ~$90B. MicroStrategy’s bitcoin holdings far outpace other corporate treasuries, holding 12x more than miners like Marathon Digital (MARA) and 34x more than Tesla (TSLA).

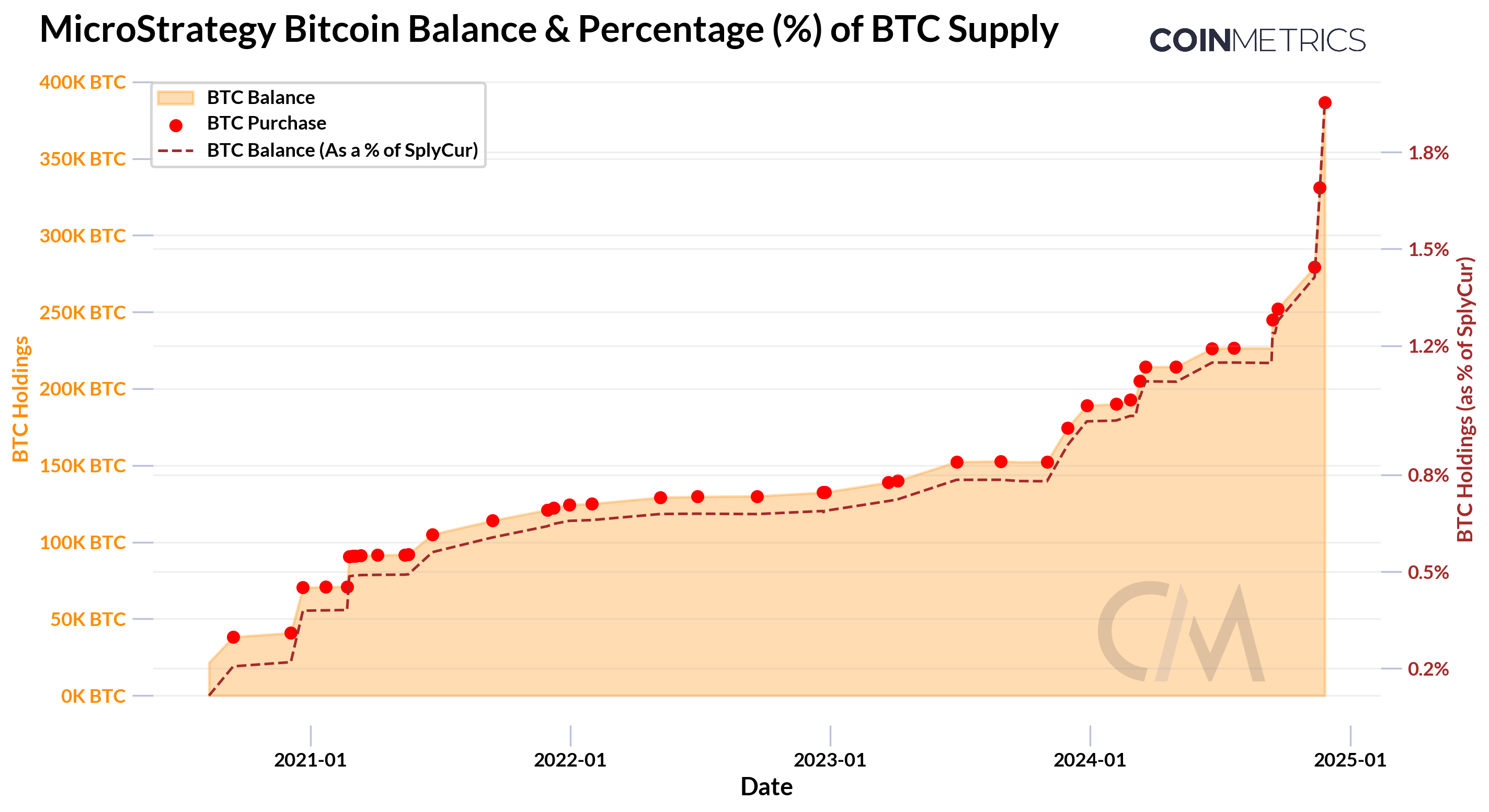

Source: Coin Metrics Network Data Pro & BitBo Treasuries

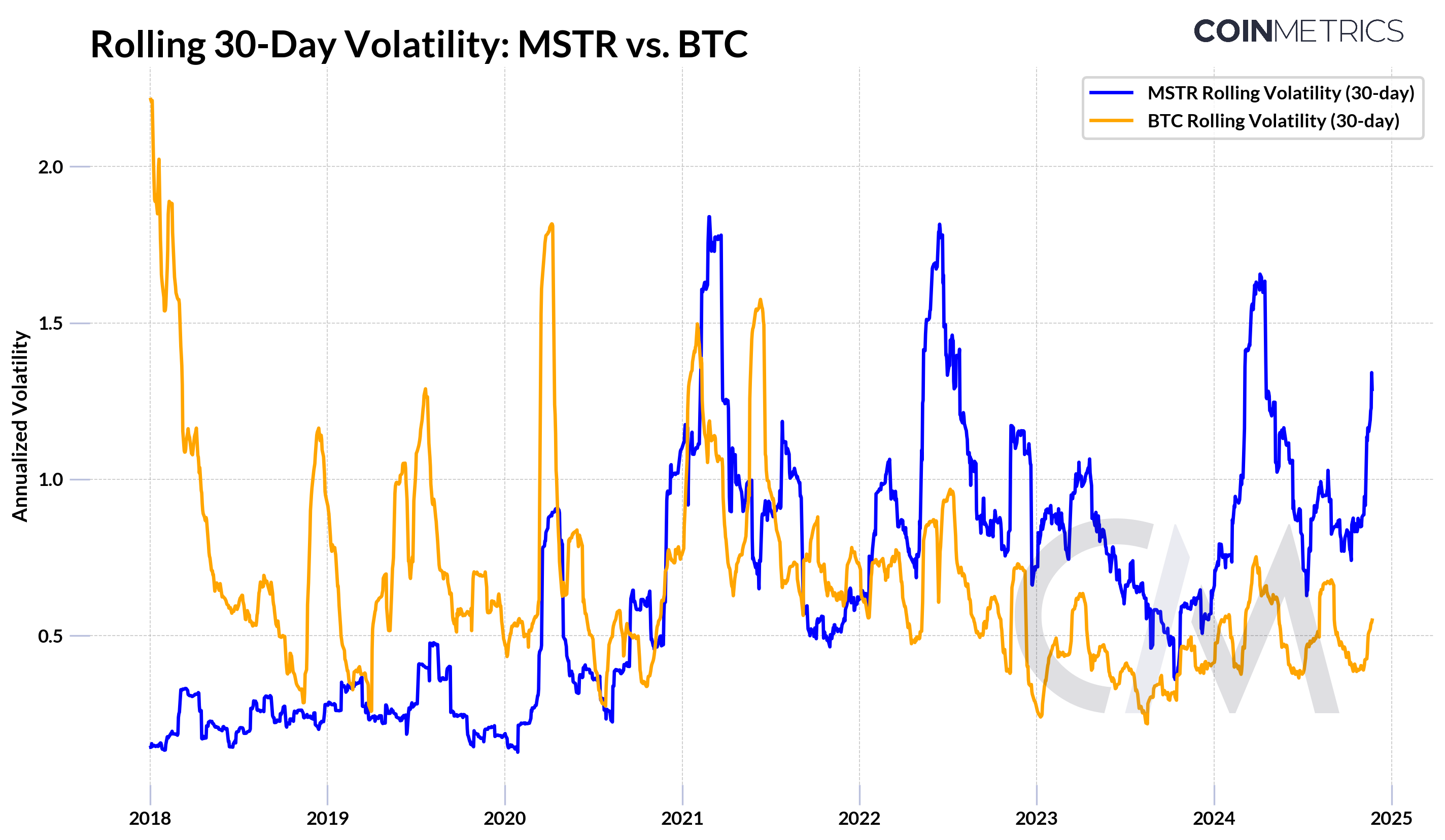

With their most recent purchase of 55,500 BTC on November 24th, MicroStrategy now holds 386,700 BTC at an average cost basis of $56,761, representing ~1.9% of Bitcoin’s current supply. Only Bitcoin spot ETFs surpass this, collectively holding ~5.3% of the supply—three times more than MicroStrategy. This strategy has effectively transformed MicroStrategy into a Bitcoin investment vehicle, serving as a leveraged play on Bitcoin. Michael Saylor has himself described the company as a “treasury operation securitizing Bitcoin, offering 1.5x to 2x leveraged equity.” As shown in the chart below, MicroStrategy’s performance relative to Bitcoin reflects this approach, amplifying gains during rallies and losses during downturns.

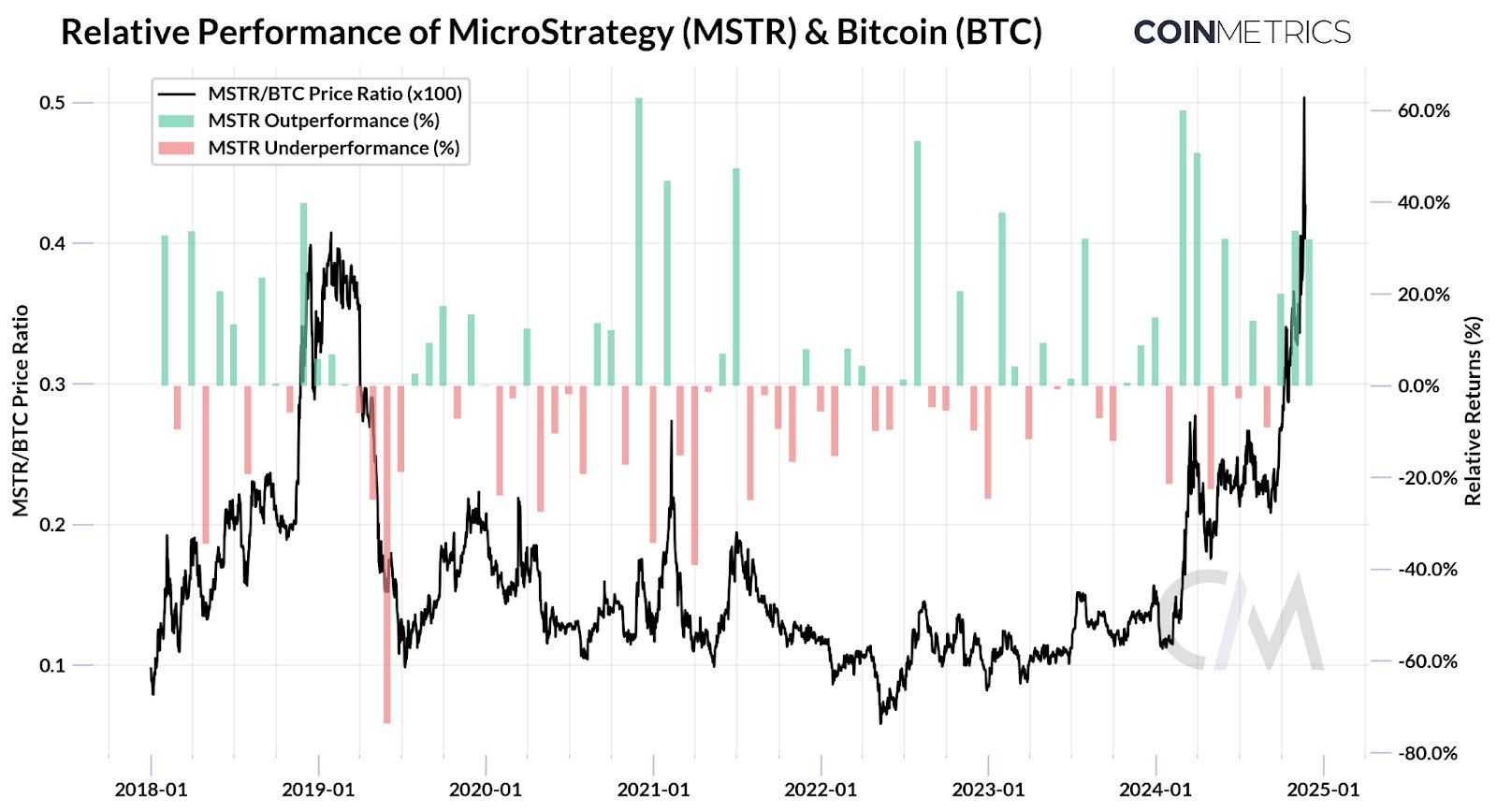

Source: Coin Metrics Reference Rates & Google Finance

This leveraged approach inherently drives higher volatility for MSTR compared to BTC, often amplifying BTC’s price movements by 1.5x to 2x. Beyond its Bitcoin exposure, MicroStrategy’s stock price is also influenced by broader equity market trends and investor sentiment toward Bitcoin, making it a high-risk, high-reward proxy for the asset’s performance.

Source: Coin Metrics Market Data Feed & Google Finance

How is MicroStrategy able to fund its massive Bitcoin purchases? The cornerstone of its strategy lies in borrowing money to buy bitcoin by issuing convertible bonds. These are a type of fixed-income instrument that act as a hybrid between debt and equity, which can be converted into a set number of the company’s shares at a future date and predetermined price.

By offering these convertible notes in fixed-income markets or directly to institutional investors, MicroStrategy has been able to raise cash to scale its Bitcoin holdings rapidly, often with remarkably low borrowing costs. These bonds are attractive to investors because they offer the potential for equity conversion at a higher price than the issuance price, effectively functioning as a call option with demand further amplified in bull markets MicroStrategy’s growing Bitcoin treasury. This creates a reflexive loop: higher BTC prices drive a higher premium on MSTR shares, enabling the company to issue more debt or equity, which funds additional BTC purchases. These purchases add to buying pressure, further lifting Bitcoin prices—and the cycle continues, reinforcing itself in a bull market.

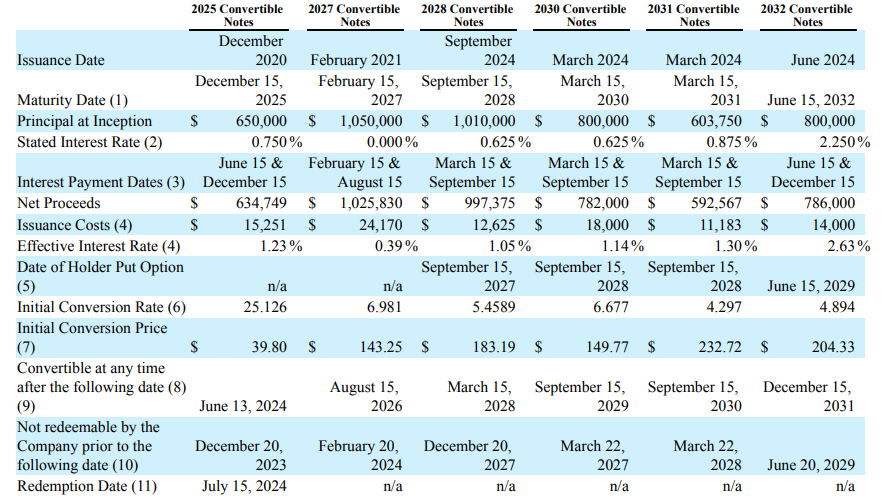

Source: Microstrategy Q3 2024 Earnings

The table above highlights MicroStrategy’s outstanding convertible notes, which mature between 2025 and 2032. They also recently raised $3B through another convertible bond offering due in 2029 with a 0% interest rate and 55% conversion premium , bringing its total outstanding debt to over $7.2B.

While their strategy has thus far brought tremendous success, one question remains: “What could go wrong? Is this another bubble waiting to burst?” With MicroStrategy’s market capitalization near ~$90B and their Bitcoin holdings valued at ~$37.6B, the company now trades at a significant premium of ~2.5x (250%) to its net asset value (NAV). In other words, MicroStrategy’s shares are priced at 2.5 times the value of their underlying Bitcoin treasury. This steep valuation premium has drawn scrutiny from market participants, raising questions about how long it can remain elevated and the potential consequences if it were to collapse or turn negative.

Participants are also attempting to take advantage of the premium on MSTR equity by shorting MSTR stock and buying BTC as a hedge. The stock has attracted ~11% in short interest, reducing from ~16% in October as some short positions are closed out. To assess the risk of MicroStrategy potentially liquidating part of its bitcoin holdings and the implications of a declining MSTR/BTC price and NAV premium, turning to the health of its legacy software business may provide a better idea of its ability to service these levels of debt.

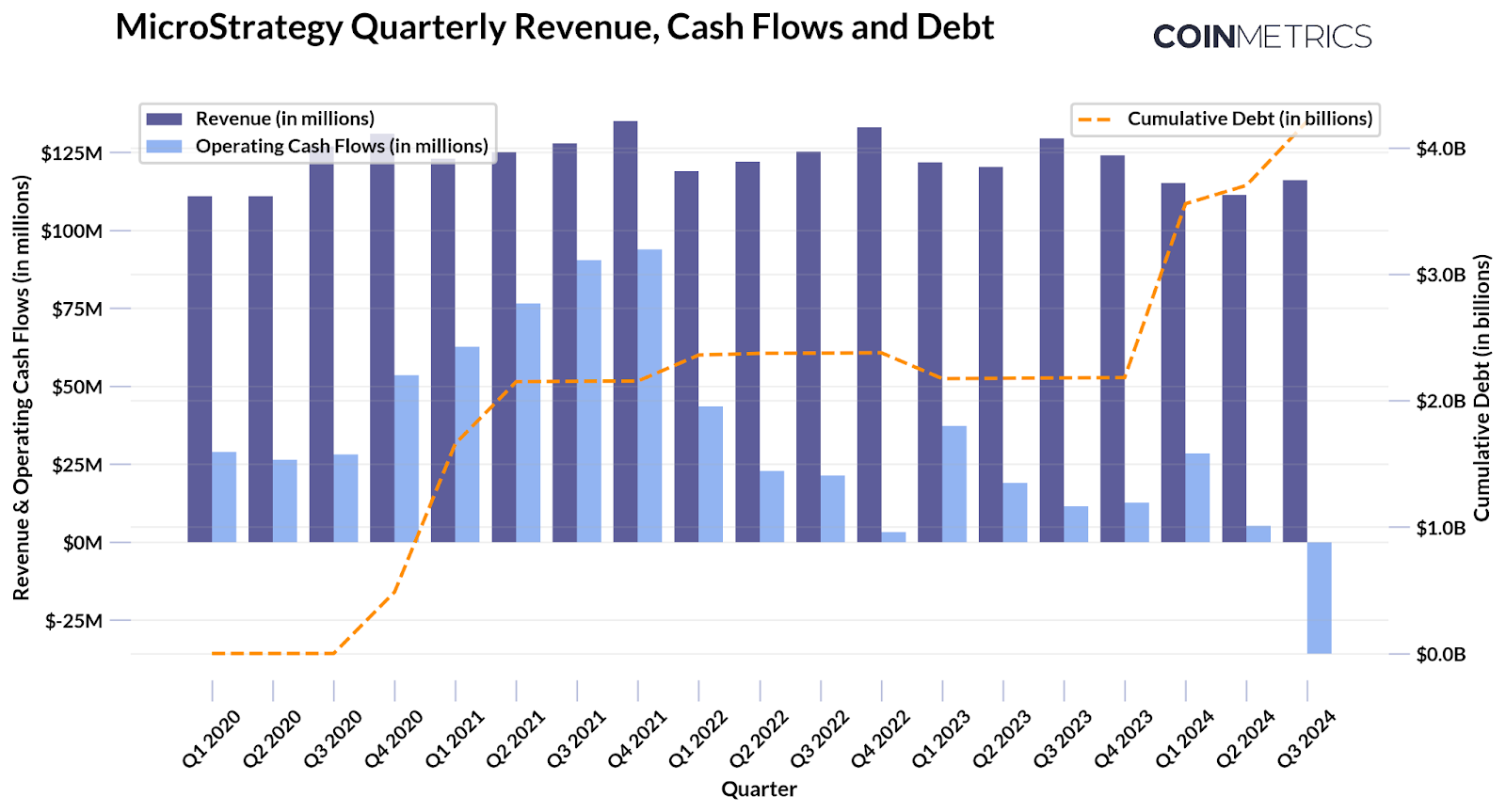

Source: MicroStrategy Quarterly Earnings as of Q3 2024

While quarterly revenues for the legacy business have been relatively steady since 2020, operating cash flows show a declining trend. Meanwhile, cumulative debt has grown significantly since 2020 reaching $7.2B, driven by the issuance of convertible notes to fund Bitcoin acquisitions, speeding up during bullish market conditions. This reflects the company’s reliance on Bitcoin’s appreciation to maintain financial stability. Despite this, the relatively low interest costs on these bonds are likely serviceable by the software business. If bondholders convert their notes into equity at higher share prices upon maturity, much of the debt would resolve without requiring cash repayment. However, if market conditions deteriorate and the premium on MicroStrategy’s shares erodes, the company may need to explore alternative strategies to meet its obligations

MicroStrategy’s bold approach highlights Bitcoin’s potential as a corporate reserve asset. By leveraging its large Bitcoin chest, the company has amplified its market performance, establishing itself as a unique proxy to BTC. However, this strategy carries inherent risks tied to Bitcoin’s price volatility and the sustainability of equity premiums, warranting closer attention as market conditions evolve. MicroStrategy’s model could inspire broader adoption—not only among corporations but potentially at the sovereign level, further cementing Bitcoin’s role as a store of value and superior reserve asset.

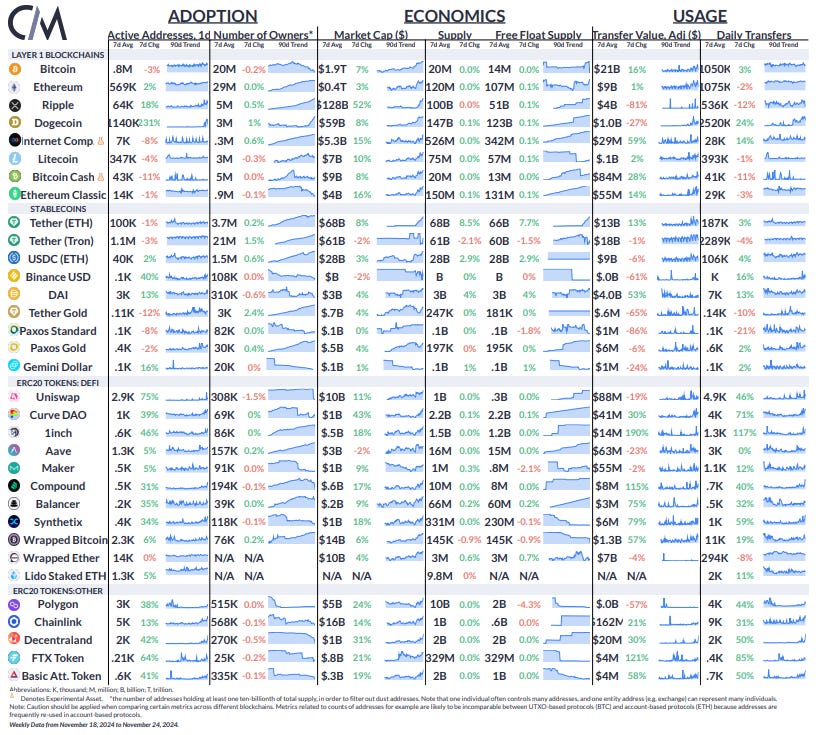

Source: Coin Metrics Network Data Pro

Over the past week, Ripple’s (XRP) market capitalization grew by 52%, reaching $128B. Daily active addresses for Dogecoin (DOGE) rose by 231%, while activity increased across the board for several ERC-20 tokens.

This week’s updates from the Coin Metrics team:

-

Be sure to check out our new Ethereum Overview report, diving into ETH’s historical investment performance, adoption, supply dynamics and more.

-

Follow Coin Metrics’ State of the Market newsletter which contextualizes the week’s crypto market movements with concise commentary, rich visuals, and timely data.

As always, if you have any feedback or requests please let us know here.

Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you’d like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.